Comprehensive guide on taxation of foreign-owned LLCs in the United States: when real taxes apply, which forms to use, and which risks to avoid.

The taxation of foreign-owned LLCs in the United States is one of the topics that generates the most questions among those who create a company in the U.S. without residing in the country. Many foreign owners wonder whether they actually need to pay federal taxes, file personal reports, or comply with additional obligations beyond the basic IRS forms.

The confusion is completely understandable. It is common to form an LLC to sell globally, charge in dollars, or access international platforms and receive simplified messages such as “if you don’t generate revenue in the U.S., you don’t pay taxes” or “you only need to file one form per year.” These statements may be partially correct in certain scenarios, but they are dangerously incomplete when the LLC generates effectively connected income (ECI), operates in certain states, or the owner incurs personal obligations such as FBAR or FATCA.

For this reason, discussing the taxation of foreign-owned LLCs in the United States is not just about federal taxes. It involves understanding when an LLC shifts from a purely informational framework to a scenario of real taxation, which personal responsibilities may arise, which state-level obligations may apply, and how to comply correctly to avoid penalties, banking restrictions, or operational issues.

In this guide, you will find a clear, practical, and technically accurate overview to understand when a foreign-owned LLC must pay taxes in the U.S., which forms apply in each case, and how to manage full compliance safely.

Tax forms for foreign-owned LLCs in the U.S.

Understanding the correct forms is at the core of the taxation of foreign-owned LLCs in the United States, since each combination of factors can trigger completely different obligations.

A foreign-owned LLC does not have a single tax framework. Its obligations depend on several key factors:

- The LLC’s tax classification with the IRS

- The existence or absence of effectively connected income (ECI)

- Activities, employees, or presence in the U.S.

- Number of owners

- Tax elections made

Understanding this combination is essential to avoid filing incorrect forms or assuming there is no obligation when one actually exists.

Applicable forms depending on the scenario

| LLC Scenario | Tax classification | Main forms | Key observations |

|---|---|---|---|

| Single-member foreign-owned LLC without ECI (default) | Disregarded entity | Form 5472 + Form 1120 pro forma | Informational obligation even without income |

| Single-member foreign-owned LLC with ECI | Disregarded entity | Form 5472 + applicable income tax return | May generate federal tax |

| LLC with two or more foreign partners | Partnership | Form 1065 + Schedule K-1 | Each partner reports their share |

| LLC that elected to be taxed as a corporation | C Corporation | Form 1120 | Regular corporate taxation |

| LLC with employees in the U.S. | Employer | Employment forms (941, W-2, etc.) | Ongoing obligations |

| LLC with activity in specific states | Variable | State reports + franchise tax | May apply even without income |

Form 5472 + Form 1120 pro forma: core obligation

For most single-member foreign-owned LLCs (foreign-owned single-member LLC) that have not elected to be taxed as a corporation, the main obligation before the IRS is to file Form 5472 along with a pro forma Form 1120.

This obligation exists even if the company had no income or business activity. The purpose is to report reportable transactions with foreign related parties, primarily the owner.

The pro forma Form 1120 does not calculate tax. It functions as a “cover page” to submit Form 5472 within the IRS system.

When this obligation is triggered

It is required when, during the tax year, at least one reportable transaction occurred between the LLC and its foreign owner or related entities.

Typically reportable transactions

- Capital contributions from the owner to the LLC

- Withdrawals or distributions of money

- Loans between the owner and the company

- Payment of personal expenses with LLC funds or vice versa

- Transfers with other companies within the same group

Even a single transaction may be enough to trigger the obligation.

Failure to comply may result in very significant penalties for each year not filed.

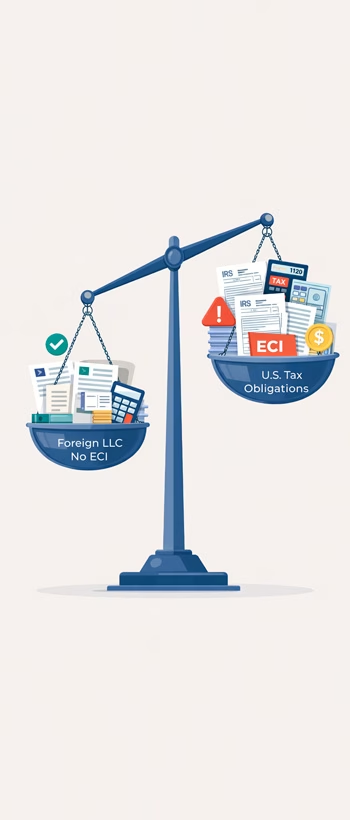

When ECI exists: shift in tax scenario

The existence of effectively connected income (ECI) with the United States radically changes the LLC’s tax treatment.

In this case, the company moves from a purely informational framework to potentially being subject to federal income tax like any business operating in the U.S.

The concept of ECI is based on whether the activity constitutes a trade or business in the United States, regardless of the owner’s residence.

Main consequences of having ECI

- Obligation to report income and expenses to determine net profit

- Potential payment of federal income tax

- Additional reporting requirements

- Potential state obligations depending on the activity

Common indicators of ECI

- Provision of services physically within the United States.

- Inventory stored or distributed from U.S. territory

- Offices, employees, or dependent agents in the country

- Ongoing business activity targeting the U.S. market

Not all income from U.S. clients constitutes ECI. The analysis depends on the nature of the activity, how the service is performed, and potential tax treaties.

Forms for LLCs with multiple owners

When an LLC has two or more members and has not elected to be taxed as a corporation, the IRS classifies it by default as a partnership.

Under this regime, the entity generally does not pay income tax at the corporate level. Instead, the results are “passed through” to the partners.

Main obligations

- File Form 1065 (U.S. Return of Partnership Income)

- Issue a Schedule K-1 to each partner showing their share of income, losses, and deductions

- Each foreign owner must report their share according to the rules applicable to non-residents

If there is ECI, specific withholding may apply to the share of foreign partners, along with additional reporting obligations.

LLC taxed as a corporation

An LLC may voluntarily elect to be taxed as a C Corporation by making a tax election with the IRS. In that case, it ceases to be treated as a pass-through entity and becomes subject to the full corporate tax regime.

Main implications

- Filing Form 1120 (Corporate Income Tax Return)

- Payment of tax on net income at the corporate level

- Potential double taxation if dividends are distributed to the foreign owner

- Application of withholding on dividends according to law or tax treaties

This regime may be advantageous in certain scenarios but involves greater administrative and tax complexity.

Employment forms

If the LLC hires employees within the United States, the level of compliance increases significantly. At that point, the company assumes ongoing obligations as an employer before the IRS and other federal and state agencies.

These obligations do not depend on the owner being foreign, but on having workers within U.S. territory.

Among the most common reports are:

- Quarterly payroll tax filings (e.g., wages and withholdings)

- Annual forms reporting income paid to each employee

- Reports related to Social Security and Medicare

- Potential federal and state unemployment obligations

Additionally, there may be further requirements depending on the state where employees work, such as mandatory insurance, state withholdings, or specific labor registrations.

Failure to comply with these obligations may result in cumulative penalties, interest, and difficulties in continuing to operate legally with employees in the U.S.

A U.S. LLC with a foreign owner is not defined by whether it pays taxes or not, but by when its operations, filings, and personal obligations trigger a full tax regime and real compliance risks.

Associated state obligations

Even if an LLC does not generate income in the United States or its main activity takes place abroad, the state where it is registered — and, in some cases, other states where it operates — may require mandatory annual payments and filings.

These obligations exist to keep the company active and in good legal standing, not necessarily because there are economic benefits.

The most common include:

- Franchise tax or state franchise tax

- Annual minimum tax regardless of income

- Annual report or entity renewal (annual report)

- Administrative fees for maintaining the registration

The amount and rules vary significantly depending on the state. Some states have low costs and simple requirements, while others impose higher tax burdens or multiple obligations even without economic activity.

If the LLC conducts operations in a state different from its state of formation — for example, having clients, inventory, an office, or employees — it may be required to register as a foreign entity in that state and comply with its local taxes and reporting requirements.

Failure to comply at the state level may result in:

- Loss of good standing (active status)

- Cumulative fines and charges

- Administrative suspension or dissolution of the LLC

- Difficulties in opening or maintaining bank accounts and commercial contracts

For this reason, state compliance must be analyzed together with federal compliance and not treated as a minor requirement.

Personal obligations of the foreign owner: FBAR and FATCA

In addition to the LLC’s obligations, the foreign owner may have personal financial reporting responsibilities before U.S. authorities when they own or control accounts outside the United States. These obligations do not replace those of the company and may exist even if the LLC has no income or does not pay federal taxes.

FBAR (FinCEN Form 114): reporting foreign financial accounts

The FBAR (Report of Foreign Bank and Financial Accounts) is an annual report required under the Bank Secrecy Act when a U.S. person (including certain foreign owners with U.S. reporting obligations) has a financial interest in or signature authority over financial accounts outside the United States whose aggregate maximum value exceeds USD 10,000 at any time during the calendar year.

Key aspects:

- It is a personal obligation, not an LLC obligation.

- It is filed electronically with FinCEN using FinCEN Form 114.

- The USD 10,000 threshold is calculated based on the combined total of all foreign accounts.

- It does not depend on whether the accounts generated income or taxes.

- The standard deadline is April 15, with an automatic extension to October 15.

Which accounts must be reported in the FBAR

Financial accounts held outside the U.S. over which there is direct or indirect ownership or authority must be included, for example:

- Personal bank accounts abroad

- Foreign corporate accounts where the individual is an owner or has signature authority

- Investment, brokerage, or fund accounts outside the U.S.

- Certain payment accounts or electronic wallets, if they qualify as financial accounts

- Trust structures or entities where there is substantial control

Failure to report required accounts may result in significant penalties, even without deliberate intent. Fines may increase substantially if the omission is considered willful.

FATCA: reporting foreign financial assets (Form 8938)

FATCA (Foreign Account Tax Compliance Act) establishes a reporting regime separate from FBAR. It requires certain taxpayers subject to U.S. tax obligations to report foreign financial assets using Form 8938, typically attached to the federal tax return.

Main characteristics:

- It is filed with the IRS as part of the tax return.

- It applies when the value of foreign financial assets exceeds specific thresholds, which vary depending on marital status and residence.

- It includes financial accounts and other assets held outside the U.S., such as interests in foreign entities or financial instruments.

- It functions as a complement to the international financial information exchange system.

It is important to note that FATCA does not replace FBAR. Both reports may be required simultaneously if their respective criteria are met.

Key differences between FBAR and FATCA

Although both aim to provide transparency regarding foreign financial assets, they present fundamental differences:

- Receiving authority: FBAR is filed with FinCEN; FATCA is filed with the IRS.

- Form: FBAR uses FinCEN Form 114; FATCA uses Form 8938.

- Type of information: FBAR focuses on financial accounts; FATCA covers accounts and other foreign financial assets.

- Thresholds: reporting thresholds are not the same and are calculated differently.

- Filing method: FBAR is submitted separately from the tax return; FATCA is attached to it.

- Penalties: each regime has its own system of penalties and enforcement.

Since these obligations are personal and may coexist with LLC obligations, it is essential to evaluate them together within the foreign owner’s overall tax planning.

Filing method with the IRS

Complying with tax obligations not only involves filing the correct forms but also submitting them through the appropriate channel according to current IRS regulations and retaining proof of filing. For foreign-owned LLCs, this point is critical because certain informational forms — especially those related to non-resident owners — have specific rules regarding submission, signature, and acceptance.

Electronic filing (e-file) vs. paper filing (paper filing)

The IRS requires or prioritizes electronic filing for most corporate and partnership returns, but not all foreign-owned LLC scenarios fit within e-file.

In general terms:

- Form 1120 (corporations): typically must be filed electronically through authorized providers, except in limited cases.

- Form 1065 (partnerships): also usually requires e-file; entities with a larger number of partners are required to file electronically.

- Form 7004 (extension): can be filed electronically and is recommended to ensure immediate confirmation.

- Form 5472 with 1120 pro forma (single-member foreign-owned LLC): often filed in paper format, following specific IRS instructions.

Submitting a form through the wrong channel may result in rejection or the filing being considered not submitted.

Particularities of Form 5472 with 1120 pro forma

For single-member foreign-owned LLCs treated as disregarded entity, the 5472 + 1120 pro forma package often requires special attention:

- Form 1120 is used solely as a vehicle to attach Form 5472.

- It must be completed with only basic identification information.

- Filing may be done by mail to specific addresses designated by the IRS (which may change periodically).

- It is essential to review the current Form 5472 instructions each year.

Since these entities often do not have U.S. Social Security numbers, electronic filing may not be available or may be more complex.

Signature and authentication requirements

Depending on the form and the submission method:

- Electronic filings use digital authentication systems or an assigned PIN.

- Mail submissions require a handwritten signature from the authorized representative.

- The signer must have formal authority over the entity.

The absence of a valid signature may invalidate the filing.

Use of postal services and proof of delivery

When filing by mail, it is recommended to use services with delivery confirmation, such as certified mail or IRS-approved courier services.

This allows you to demonstrate that the return was submitted on time in case of disputes or processing delays.

Frequent changes in instructions and addresses

The IRS periodically updates:

- Mailing addresses

- Procedures for foreign entities

- Documentation requirements

- Availability of e-file for certain forms

Therefore, relying on information from previous years may lead to unintentional errors.

Operational recommendations for foreign-owned LLCs

- Review the official instructions for the relevant form each year

- Confirm whether e-file is required or if paper filing is allowed

- File extensions when necessary

- Keep delivery receipts or proof of submission

- Maintain complete copies of everything filed

A correct filing strategy not only ensures formal compliance but also significantly reduces the risk of penalties, additional requests, or future issues with the IRS.

Risks of non-compliance

Non-compliance in a U.S. LLC with foreign owners should not be seen as a minor “paperwork” issue or a simple administrative omission. Depending on the form omitted, the time elapsed, whether tax was due, and whether the owner also failed to meet personal obligations, the consequences can escalate rapidly at the tax, banking, operational, and reputational levels.

Additionally, in this context it is useful to distinguish between four types of risk: penalties for LLC informational forms, penalties for unreported or unpaid federal tax, personal penalties for international financial reporting, and state and operational consequences. Each operates differently and may accumulate with the others.

Risk from non-compliance with LLC informational forms

When a foreign-owned single-member LLC fails to properly file Form 5472 with Form 1120 pro forma, the IRS may impose a specific penalty for informational non-compliance. This is not a minor detail: it is one of the most significant sanctions for LLCs with foreign owners and may apply even when the company has no profits.

In practical terms, this risk includes:

- Penalty for failing to file the form on time

- Penalty for submitting incomplete or materially incorrect information

- Risk of additional penalties if not corrected after an IRS notice

- Higher likelihood of review if multiple omissions accumulate

The critical point is that many LLCs believe that “no income means no problem,” when in reality the main risk may lie precisely in not reporting transactions with the owner or related parties.

Risk from unreported or unpaid federal tax

If the LLC generates ECI (effectively connected income with the United States) or falls under a regime where federal income tax actually applies, it is no longer just an informational omission. In that case, more serious tax consequences may accumulate:

- Interest on unpaid tax from the due date

- Penalties for late filing of the tax return

- Penalties for late payment of tax

- Adjustments for expenses or deductions not accepted if documentation is insufficient

- Greater exposure to audits and supporting documentation requests

Here, the risk is not just the penalty. There may also be a higher tax assessment than expected if the taxpayer cannot properly support the adopted position.

Personal risk related to FBAR and FATCA

When the foreign owner is subject to personal international financial reporting obligations, non-compliance can open a completely separate front from that of the LLC.

In particular:

- FBAR has its own penalty regime

- Penalties may vary depending on whether the omission was non-willful or willful

- FATCA/Form 8938 also carries independent penalties

- The absence of tax due does not necessarily eliminate the risk of penalties for failure to report

This is especially delicate because many owners focus all their attention on the company and overlook the fact that certain obligations fall on them personally.

State and corporate maintenance risk

At the state level, non-compliance can also generate significant effects even if no federal tax is due. Depending on the state, an LLC may be exposed to:

- Penalties for failing to file annual reports

- Charges for not paying franchise tax or minimum taxes

- Loss of good standing

- Administrative suspension or dissolution of the entity

- Difficulties proving that the company remains active and compliant

This point is especially sensitive for digital businesses that depend on banks, payment processors, marketplaces, or partners that review the legal status of the company.

Banking, operational, and commercial risk

Beyond the strictly tax-related aspect, non-compliance can affect the LLC’s ability to operate normally.

Among the most common consequences are:

- Requests for additional documentation from the bank

- Internal compliance restrictions

- Freezing, closure, or enhanced review of accounts

- Issues with payment processors or international platforms

- Difficulties in due diligence processes, business sales, or onboarding new partners

In practice, many companies feel the operational impact before the tax impact, especially when a financial institution detects inconsistencies or lack of documentation.

Cumulative risk: the real problem

The biggest mistake is analyzing each obligation separately. In reality, non-compliance tends to accumulate. An LLC may simultaneously:

- Fail to file a mandatory informational form

- Have exposure to federal tax due to ECI

- Neglect state-level obligations

- Have the owner out of compliance with FBAR or FATCA

When this happens, the cost of remediation increases not only due to penalties and interest, but also because of technical complexity, professional fees, administrative time, and reputational risk.

For this reason, the goal should not be merely to “file something to stay current,” but to build comprehensive compliance that protects both the company and its owner.

Comprehensive compliance checklist

Proper compliance for a U.S. LLC with foreign owners is not based on “filing one form per year,” but on systematically verifying all factors that determine the actual obligations of both the entity and the owner. This checklist serves as an annual preventive control guide before the fiscal year-end or filing deadline.

1. Determine the LLC’s federal tax status

- Verify whether the LLC maintained its default tax classification or made any election (for example, an election to be taxed as a corporation).

- Confirm whether it is a single-member entity or has multiple partners.

- Identify whether structural changes occurred during the year (new partners, ownership transfers, entity conversion, etc.).

These factors determine which primary return must be filed.

2. Assess whether effectively connected income (ECI) existed

- Analyze whether the activity constitutes a trade or business in the United States.

- Review whether there was physical presence, employees, dependent agents, inventory, or services performed within the country.

- Evaluate contracts, place of service performance, and operational model.

The existence of ECI transforms a purely informational scenario into one of actual taxation.

3. Identify transactions with the owner or related parties

Especially relevant for foreign-owned single-member LLC:

- Capital contributions

- Withdrawals or distributions

- Loans between the LLC and the owner

- Cross-payment of personal or corporate expenses

- Transactions with related foreign companies

These transactions often trigger the Form 5472 requirement even without revenue.

4. Confirm federal informational and tax obligations

Depending on the scenario, it may be necessary to verify:

- Filing of Form 5472 with Form 1120 pro forma

- Partnership return (Form 1065) and issuance of K-1

- Corporate return (Form 1120) if applicable

- Withholding forms or additional reporting in case of ECI

- Employment filings if there are employees in the U.S.

Failure to file informational forms may result in significant penalties even if no tax is due.

5. Review state-level obligations

- Confirm payment of franchise tax or minimum state tax.

- File the annual report or required renewal.

- Verify whether the LLC must register as a foreign entity in other states where it operates.

- Confirm good standing status.

State compliance is independent from federal compliance and may affect the company’s operational validity.

6. Evaluate the foreign owner’s personal obligations

Depending on your overall tax and financial situation:

- Determine whether there is an FBAR obligation for foreign financial accounts.

- Assess whether FATCA reporting (Form 8938) applies.

- Analyze potential personal filing obligations related to ECI income or LLC ownership interests.

These obligations do not belong to the company, but may arise from its existence or activity.

7. Verify deadlines and extension requirements

- Identify the applicable deadline based on the entity type.

- Assess whether accounting information is complete to file on time.

- File an extension (for example, Form 7004) when necessary.

Requesting an extension does not eliminate the obligation, but reduces the risk of late filing penalties.

8. Prepare accounting and supporting documentation

- Basic financial statements for the period.

- Records of income, expenses, and transfers.

- Relevant contracts.

- Support for related-party transactions.

Proper documentation facilitates accurate preparation and supports defense in case of potential reviews.

9. Maintain records and proof of filing

- Complete copies of submitted returns.

- e-file confirmations or proof of postal delivery.

- Correspondence with the IRS or state authorities.

- Records from prior years.

Document history is essential to demonstrate compliance and respond to future inquiries.

Implementing this annual control allows you to anticipate obligations, reduce costly errors, and keep the LLC operating within a solid compliance framework at the federal, state, and personal levels.

Frequently asked questions (FAQ)

Does a U.S. LLC with a foreign owner always have to pay federal taxes?

No. The obligation to pay income tax depends mainly on whether the LLC generates effectively connected income (ECI) with the U.S. or whether it elected to be taxed as a corporation. Many LLCs operated from abroad do not have federal income tax, but they still must file mandatory informational forms. Confusing “not paying taxes” with “not filing anything” is one of the most common mistakes.

What exactly does it mean for an LLC to have ECI?

ECI means that the activity constitutes a trade or business in the United States under tax regulations. It is not determined solely by the origin of clients or payments, but by factors such as physical presence, services performed within the country, stored inventory, employees, or dependent agents. When ECI exists, the LLC or its owners may become subject to federal taxation on the net profit attributable to that activity.

If I sell services or products online from outside the U.S., does that automatically generate ECI?

Not necessarily. Many digital businesses operated entirely from abroad do not generate ECI, even if they have U.S. clients. However, the analysis depends on the actual operating model. For example, using warehouses in the U.S., hiring local personnel, or providing services in person may change the outcome.

Do I have to file Form 5472 if my LLC had no income?

Yes, in many cases. For a foreign-owned single-member LLC, Form 5472 is required when there are reportable transactions with the owner or related parties, even if there were no sales or profits. Capital contributions, withdrawals of funds, or loans may trigger the obligation.

What happens if I do not file Form 5472 or file it incorrectly?

The IRS may impose significant penalties for each year of non-compliance. In addition, if the omission is not corrected after a notice, further sanctions may apply. These penalties are based on informational non-compliance, not on whether taxes are due.

Do state obligations exist even if the LLC has no activity?

In many states, yes. Payment of franchise tax, minimum taxes, or filing the annual report is often necessary to keep the company legally active. Failure to comply may lead to loss of good standing, suspension, or administrative dissolution.

What is FBAR and why can it affect a foreign owner?

FBAR is a personal report of financial accounts outside the U.S. required when certain thresholds are exceeded and specific U.S. tax obligation criteria are met. It is not a tax or a company form, but an individual report filed with FinCEN. It may apply even if the LLC has no income or does not pay taxes.

Is FATCA the same as FBAR?

No. Although both report foreign financial assets, FATCA (Form 8938) is filed with the IRS as part of the tax return and has different thresholds and scope. It is possible to be required to file both reports simultaneously.

Can I have an LLC in the U.S. without living there or traveling to the country?

Yes, the owner’s residency does not by itself determine the company’s tax obligation. What matters is where and how the economic activity is carried out. Many LLCs are owned by non-residents who operate entirely from abroad.

Does the LLC protect the owner from personal obligations before the IRS or FinCEN?

The LLC limits business legal liability, but it does not eliminate personal tax obligations. If the owner is subject to individual reporting such as FBAR or FATCA, they must comply regardless of the entity’s limited liability.

Can I correct prior years if I failed to comply with an obligation?

Yes, there are mechanisms to regularize your situation, but the appropriate strategy depends on the type of non-compliance, the time elapsed, and whether there was any willful intent. Early remediation typically significantly reduces the risk of greater penalties and future complications.

When is it advisable to request a professional tax assessment?

When there is uncertainty about whether the LLC generates ECI, if complex transactions have been carried out, if there is activity in multiple states, or if the owner may have personal international reporting obligations. In such cases, a specialized review helps avoid errors that can become costly in the long term.

Conclusion

The taxation of foreign-owned LLCs in the United States does not follow a single rule or simplified solutions. Tax treatment depends on critical variables such as the existence of effectively connected income (ECI), the chosen tax classification, economic presence in the country, state obligations, and the owner’s personal reporting requirements.

An LLC may operate for years under purely informational obligations or, conversely, quickly transition to a fully taxable scenario if business circumstances change. Ignoring these differences can result in significant penalties, loss of legal status, banking issues, or difficulties scaling internationally.

Understanding which forms apply, when actual taxes are triggered, and how federal, state, and personal obligations interact allows you to use a U.S. LLC in a strategic and secure manner.

In an increasingly demanding regulatory environment, preventive compliance is not just a legal obligation: it is a tool for business and asset protection.

If you have a U.S. LLC and are a foreign owner, analyzing your specific situation can make the difference between minimal compliance and a secure, optimized tax structure.

A professional assessment allows you to:

- Determine whether your LLC generates or could generate ECI

- Identify applicable federal, state, and personal obligations

- Detect hidden risks before they turn into penalties

- Properly plan the international growth of your business

Taking early action reduces costs, avoids future issues, and provides clarity to operate confidently in the global market.