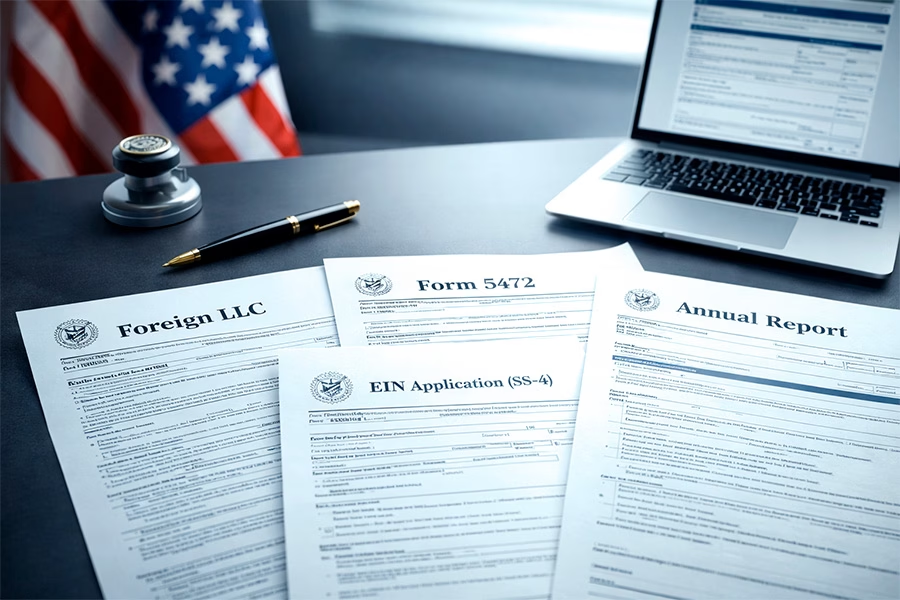

This guide on mandatory forms for foreign-owned LLCs in the U.S. specifically refers to an LLC incorporated in the United States whose owner is a foreign individual (foreign-owned U.S. LLC), even if the owner does not reside in the country and the company has no physical operations within the U.S.

Thousands of digital entrepreneurs from Latin America, Brazil, and Spain use U.S. LLCs to sell globally, receive payments in dollars, or access international platforms. However, having a company registered in the U.S. implies tax obligations with the IRS, even if the activity is conducted from abroad.

Ignoring these obligations is not a simple administrative oversight. It can result in very high fines, banking issues, account freezes, and difficulties in keeping the company active.

In this pillar guide, you will discover which forms a foreign-owned LLC in the U.S. must file, who is required to do so, when to do it, how to file them correctly, what the real IRS penalties are, and how to avoid compliance issues.

Which forms a foreign-owned LLC in the U.S. must file

The obligations depend on the LLC’s tax classification with the IRS and its ownership structure, not necessarily on generating income in the U.S. or having a physical presence in the country.

Below is a clear decision matrix for U.S. LLCs owned by nonresidents.

Forms by scenario

| LLC Situation | Tax Classification | Main Forms |

|---|---|---|

| Single-member foreign-owned LLC (default) | Foreign disregarded entity | Form 5472 + Form 1120 pro forma |

| LLC with two or more foreign partners | Partnership | Form 1065 + Schedule K-1 |

| LLC that elected to be taxed as a corporation | C Corporation | Form 1120 |

| LLC with employees in the U.S. | Employer | Payroll forms (941, W-2, etc.) |

| LLC with effectively connected income (ECI) | According to tax election | May trigger federal taxes |

Form 5472 + Form 1120 (Pro Forma): key obligation

For most single-member foreign-owned LLCs, the main annual requirement is to file Form 5472 together with a pro forma Form 1120.

This report discloses transactions between the LLC and its foreign owner or related parties, even if there has been no significant business activity.

It must be filed when there are transactions such as:

- Capital contributions

- Transfers of funds between the owner and the LLC

- Loans or payments between related parties

- Certain internal financial transactions

Form 1065 and Schedule K-1: multi-member LLCs

If the LLC has two or more members, the IRS treats it by default as a partnership. In this case, it must file Form 1065, which reports the company’s activity, and issue a Schedule K-1 to each partner with their share of the results.

Form 1120: LLC taxed as a corporation

If the LLC elects to be taxed as a C Corporation through a tax election, it must file Form 1120, just like any U.S. corporation.

Payroll forms if there are employees in the U.S.

If the LLC hires personnel within the United States, it must comply with federal payroll obligations, including periodic filings and annual reports.

Who is required to file these forms

U.S. LLCs owned by foreign individuals (non-resident owners)

Any LLC registered in the U.S. whose owner is not a U.S. tax resident may be required to file informational reports, even if it operates entirely from abroad.

LLC with no activity or no income

A common belief is that if the company has no income, nothing needs to be filed. However, many foreign-owned LLCs are still required to submit informational forms even if they have not generated profits.

LLCs used for international digital businesses

E-commerce, SaaS, affiliate, online consulting, or remote service businesses often fall under these obligations, even without U.S. clients.

When must they be filed

Standard deadline

For most LLCs with foreign owners that file Form 5472 and pro forma Form 1120, the general deadline is April 15 if the tax year aligns with the calendar year.

Available extensions

An extension can be requested using Form 7004, which extends the filing deadline but does not eliminate the obligation to file later.

Consequences of late filing

Late filing may result in very high automatic penalties and formal IRS notices.

How to file correctly

Prerequisites

Before filing, the LLC must have:

· Valid EIN issued by the IRS

· Basic financial information for the year

· Foreign owner details

· Proper accounting records

Filing procedure

Depending on the form, filing may be done electronically or by mail. In the case of Form 5472 with pro forma Form 1120, it is generally submitted through specific methods indicated by the IRS.

Common mistakes

· Believing there is no obligation due to lack of income

· Not requesting an extension on time

· Lack of accounting records

· Incorrect tax classification of the LLC

What is the risk of non-compliance

IRS penalties

Non-compliance may result in very high fines for each unfiled year, in addition to interest and additional requirements.

It may also affect the ability to operate with banks, payment processors, and global platforms.

Impact on international operations

Lack of compliance may lead to account freezes, cancellation of financial services, or difficulties in keeping the company in good standing.

How much the penalties can cost

Penalties may include:

· Significant fines for unfiled forms

· Cumulative penalties for each year of non-compliance

· Professional remediation costs

· Additional legal and financial risks

A foreign LLC is not outside the scope of the IRS simply because it is located outside the U.S.: if you generate income or activity in the country, formal tax obligations may exist.

Final compliance checklist for foreign-owned LLCs

Before closing each fiscal year, verify:

✔ Whether the LLC had transactions with its owner

✔ Which forms apply based on its structure

✔ Applicable deadlines

✔ Basic accounting documentation

✔ Whether an extension needs to be requested

Frequently Asked Questions (FAQ)

What exactly is considered a foreign-owned U.S. LLC?

It is an LLC formed under the laws of a U.S. state whose direct or indirect owner is an individual or entity that is not a U.S. tax resident. For IRS purposes, many of these LLCs are treated by default as disregarded entities if they have a single owner, meaning the entity is ignored for income tax purposes, but not for informational reporting obligations.

Do I need to file forms if my LLC had no income or activity?

Often yes. In the case of a single-member foreign-owned LLC, the obligation to file Form 5472 + pro forma Form 1120 is triggered when there are reportable transactions with the owner or related parties. These transactions include capital contributions, withdrawals, loans, expense payments, or transfers of funds, even if the economic result was zero.

What counts as a “reportable transaction” for Form 5472?

It includes, among others, contributions of funds from the owner to the LLC, withdrawals by the owner, loans between related parties, payments for services between related entities, and transfers that affect the company’s financial position. It is not limited to sales or operating revenue.

What is the difference between Form 5472, pro forma 1120, 1065, and 1120?

5472 + pro forma 1120: for single-member foreign-owned LLCs (disregarded entity).

1065 + K-1: for LLCs with two or more members (partnership).

1120: for LLCs that elected to be taxed as a C corporation.

Each combination corresponds to the tax classification chosen or assigned by the IRS.

What is the deadline to file Form 5472 with pro forma Form 1120?

Generally April 15 if the tax year aligns with the calendar year. If an extension is requested using Form 7004, the deadline is usually extended until October. It is essential to file the extension before the original due date.

What is the penalty for not filing Form 5472?

The base penalty is USD 25,000 per year and per form not filed or filed incorrectly. If non-compliance continues after an IRS notice, additional penalties may be applied for successive periods, which can significantly increase the total cost.

Can I file these forms electronically?

It depends on the form. Forms 1065 and 1120 can be filed electronically in many cases. Form 5472 with pro forma Form 1120 for foreign-owned U.S. LLCs generally has specific submission requirements that must be verified each year according to current IRS instructions.

Do I need an EIN if I do not live in the U.S.?

Yes. The EIN is essential to file returns, open business bank accounts, work with payment processors, and comply with federal tax obligations. It can be obtained without having a U.S. Social Security Number.

What happens if my LLC has income only from outside the U.S.?

Even if the income comes from abroad, the LLC may have informational obligations with the IRS due to its status as a U.S. entity. Taxation will depend on factors such as the owner’s tax residency, tax treaties, and the entity’s classification.

Does having an LLC automatically mean paying federal taxes?

Not necessarily. Many foreign-owned LLCs do not pay federal income tax if they do not have effectively connected income (ECI) in the U.S. However, the obligation to report is independent of the obligation to pay taxes.

What operational risks exist if I do not comply with these obligations?

In addition to fines, non-compliance may lead to loss of access to banking services, payment processor restrictions, difficulties renewing state registrations, issues with business partners, and increased exposure to audits.

How can I be sure which forms apply to my case?

You must analyze the ownership structure, number of members, tax elections made, type of transactions with the owner, and the existence of employees. Since an error can lead to significant penalties, a professional review is usually the safest way to determine the exact obligations.

Conclusion

Having an LLC in the United States as a foreigner offers significant advantages for operating globally, but it also implies complying with specific tax obligations with the IRS.

Understanding which forms apply to your structure and filing them on time is essential to avoid penalties, protect your company, and maintain access to the international financial system.

An LLC that keeps its compliance in order conveys trust, stability, and allows scaling with legal certainty.

If your U.S. LLC has foreign owners, reviewing your tax obligations annually is not optional: it is a strategic decision to protect and grow your business.

If you have an LLC in the U.S. and do not reside in the country, a professional review can help you confirm which forms you must file and avoid penalties before issues arise.