If you have an LLC in the United States and do not reside there, you have likely heard a repeated idea many times: “since you are a non-resident, you don’t pay taxes in the U.S.” The problem is that this statement, although sometimes partially true, is often incomplete and can lead to costly mistakes.

The confusion is understandable. Many people create a U.S. LLC to sell services, run a digital business, receive payments in dollars, or access international platforms, and in this process, they receive simplified information that mixes tax, immigration, and corporate concepts as if they were the same. This gives rise to the myth that having an LLC as a foreigner automatically means not paying taxes or filing almost anything.

The reality is more complex. In some cases, a non-resident’s LLC may indeed not be subject to federal income tax. But this does not mean it is always the case, nor that there are no important obligations. Everything depends on factors such as the existence of Effectively Connected Income (ECI), the LLC structure, the actual business activity, and the required forms for the company and owner.

In this guide, we will clarify when a non-resident LLC truly does not pay taxes, when U.S. taxation may arise, and which obligations remain even when the tax is zero. We will also cover key concepts such as ECI, Form 1040NR, and BOIR, so you can differentiate a legitimate tax advantage from a dangerous myth.

Quick answer: when you pay taxes and when you don’t

For a direct answer, the reality is as follows: having an LLC in the United States as a non-resident does not automatically mean paying federal income tax. In many cases, especially when the business is operated entirely from abroad, there may be no federal tax obligation.

However, the decisive factor is not the owner’s nationality nor the state where the company was registered, but whether the activity generates Effectively Connected Income (ECI) in the United States. When ECI exists, the scenario changes completely, and tax obligations similar to a local business may arise.

Furthermore, even when no tax is due, a non-resident LLC almost always retains important obligations, such as filing informational forms, complying with regulatory requirements, and maintaining active status with federal and state authorities.

Therefore, the correct question is not “Do foreigners pay taxes with an LLC?” but rather “Does my activity create tax obligations in the U.S.?”

Most common case: no federal tax

The most frequent scenario for many foreign entrepreneurs is operating the business entirely from outside the United States. This includes providing online services, serving clients abroad, having no employees or office on U.S. territory, and not maintaining inventory within the country.

Under these conditions, the income generated is usually considered not effectively connected to the United States, meaning it is not subject to U.S. federal income tax. For example, a digital consultant working from Spain or a software developer operating from Brazil and selling to global clients generally does not generate taxable U.S. income simply by having an LLC registered there.

However, it is essential to understand that this outcome depends on the actual activity, not merely on billing in dollars or having American clients. The IRS considers where the service is performed, where business decisions are made, and whether there is a significant economic presence within the country.

Furthermore, even without federal tax, the LLC may still have mandatory informational and regulatory obligations, such as reports to the IRS or other federal agencies, in addition to state requirements to keep the company active. Therefore, “not paying tax” does not mean “no obligations.”

Case where taxes apply: ECI income

When a foreign-owned LLC generates Effectively Connected Income (ECI), the scenario changes completely. In this case, the activity is considered a U.S. trade or business for tax purposes, triggering federal taxation on the net profit attributable to that operation.

The concept of ECI does not depend on where the company is registered or the owner’s nationality, but rather on where the business is economically conducted. The IRS assesses whether there is a substantial presence in the U.S., either physical or operational.

Some common examples that may generate ECI include:

- Providing services physically within the U.S.

- Employees or contractors operating in U.S. territory

- Offices, branches, or dependent agents in the country

- Inventory stored or distributed from the U.S.

- Ongoing commercial activity targeting the U.S. market with local presence

Additionally, further obligations may arise such as:

- Specific tax withholdings for foreigners

- Individual filings for the nonresident owner

- State-level obligations depending on the location of the activity

This is where the myth that a “foreign-owned LLC does not pay taxes” stops being valid.

Obligations Even Without Tax

The fact that a non-resident’s LLC has no federal income tax does not mean it is free from obligations to U.S. authorities. In many cases, compliance is primarily informational and regulatory, but it remains mandatory and can result in significant penalties if ignored.

The United States clearly distinguishes between tax liability and reporting obligations. A company may have no taxable profit and still be required to file forms, maintain records, or meet legal requirements to remain active.

This is especially important for LLCs with foreign owners, as much of the compliance involves demonstrating fiscal and operational transparency to the IRS and other agencies.

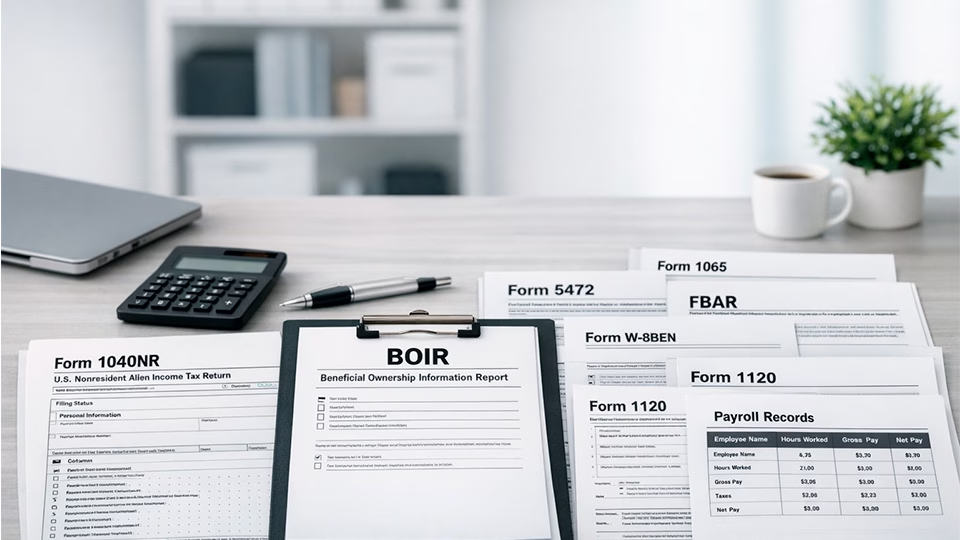

Informational Forms

The most important example is the combination of the Form 5472 with an informational statement that replicates the structure of Form 1120 (commonly called “1120 pro forma” in professional practice). This set is required for many foreign-owned single-member LLCs classified as disregarded entities.

It is important to clarify that there is no official IRS form called “1120 pro forma”. What is submitted is a Form 1120 (U.S. Corporation Income Tax Return) with the “initial” or “final” box checked, or a document that replicates its structure, serving as a vehicle to attach Form 5472, since the IRS does not allow Form 5472 to be submitted independently. The purpose is purely informational and does not imply corporate tax liability. The key example is the Form 5472 + Form 1120 pro forma set, required for many foreign-owned single-member LLCs classified as disregarded entities.

This reporting does not calculate tax. Its function is to inform the IRS about transactions between the company and its foreign owner or related parties, even if the LLC had no operational income.

Common transactions that trigger this obligation include:

- Owner capital contributions

- Withdrawals or distributions of money

- Loans between the company and the owner

- Payment of personal expenses using LLC funds

- Transfers with related companies abroad

A single transaction can be enough to trigger the annual reporting obligation.

Regulatory Reports

In addition to tax obligations, LLCs in the U.S. must comply with corporate transparency reports to other federal agencies.

One of the most relevant today is the BOIR (Beneficial Ownership Information Report) filed with FinCEN, which identifies the actual owners and individuals with control over the company.

This reporting is not related to taxes, but rather to anti-money laundering and financial transparency. Nevertheless, noncompliance can result in civil and even criminal penalties.

State Compliance

Each state where the LLC is registered, and in some cases where it operates, may require additional obligations to keep the company active.

Among the most common:

- Annual report or entity renewal

- Payment of franchise tax or minimum state tax

- Mandatory administrative fees

- Updating corporate information

These obligations exist even if the company has no revenue, employees, or activity in the U.S.

Noncompliance can lead to:

- Loss of good standing

- Accumulated fines

- Administrative suspension or dissolution

- Difficulty operating with banks and platforms

Therefore, an LLC may not owe federal taxes and still have significant legal responsibilities that must be fulfilled every year.

What it means to be a tax nonresident in the United States

Understanding what it means to be a tax nonresident in the United States is essential to determine whether a foreign individual is required to pay taxes in the country. In the U.S. tax system, tax liability does not depend solely on owning a registered company or having an EIN. It primarily depends on the person’s tax status and the source of income.

Many people believe that by not living in the United States, they are automatically outside the U.S. tax system. However, the IRS uses specific criteria to determine when a person is considered a Nonresident Alien and how their income should be treated.

Therefore, before analyzing whether an LLC pays taxes or not, it is necessary first to understand what it really means to be a tax nonresident under the U.S. system.

Difference between tax residence and immigration status

It does not depend solely on visa or citizenship

In the United States, tax residence and immigration residence are completely different concepts.

A person can:

- Hold a U.S. visa and still be a tax nonresident

- Have no visa and still become a tax resident

- Be a foreign national and have tax obligations in the U.S.

The U.S. tax system uses its own criteria to determine tax residency. The two main tests are:

Green Card Test

A person is considered a tax resident if they hold a valid Green Card, regardless of the amount of time spent inside or outside the country.

Substantial Presence Test

Tax residency can also be acquired if a person stays in the United States for a specific number of days over a three-year period.

If neither of these criteria is met, the individual is generally classified as a Nonresident Alien, meaning the U.S. tax system will only tax certain specific types of income.

For this reason, having an LLC in the United States does not automatically make the owner a tax resident, nor does it automatically mean they must pay federal tax on all their income.

Concept of Nonresident Alien

How the tax system defines it

The official term used by the U.S. tax system is Nonresident Alien (NRA). It refers to a foreign person who does not meet the requirements to be treated as a tax resident.

A Nonresident Alien:

- Is not taxed in the U.S. on worldwide income

- Is taxed only on U.S.-source or U.S.-connected income

- May be subject to specific withholding

- Must file specific forms when applicable

This classification applies to most foreign LLC owners who live permanently outside the United States and do not meet the criteria for tax residency.

Why residency does not automatically determine taxes

Importance of the source of income

In the U.S. system, the determining factor is not only who you are or where you live, but where your income comes from and how it is generated.

For nonresidents, the IRS mainly distinguishes between:

- Effectively connected income with the U.S. (ECI)

- Non-connected or foreign-sourced income

Two individuals with the same nationality and residence may have completely different tax obligations depending on the nature of their economic activity.

For example, a foreign entrepreneur operating entirely from their home country may have no federal tax, while another with operational presence in the U.S. may be subject to full taxation.

Understanding this logic helps avoid common mistakes, such as assuming that living outside the country automatically means not paying taxes in the United States.

How the LLC structure influences taxes

The way an LLC is classified for tax purposes is one of the most important factors in determining whether a foreign owner must pay taxes in the United States and how they will be calculated. Unlike many countries, in the U.S. the same legal entity can receive completely different tax treatments depending on its structure and the elections made with the IRS.

This means it is not enough to say “I have an LLC.” It is necessary to understand how the IRS views that LLC for tax purposes, because this classification determines:

- Who pays the taxes: the company or the owner

- Which forms must be filed

- Whether the income will be taxed in the U.S. or not

- Whether there is taxation at the personal level

- The type of applicable withholdings

Two legally identical LLCs can have completely different tax obligations if their classification is not the same.

Single-member LLC (disregarded entity)

Tax transparency, owner-level taxation

When an LLC has only one owner and has not made any special tax election, the IRS by default classifies it as a disregarded entity for tax purposes.

Under this regime, the company is not treated as a separate taxpayer from the owner. In practice, the LLC functions as a tax extension of the individual who owns it.

This implies that:

- The LLC does not pay federal income tax on its own

- The income is attributed directly to the owner

- Taxation depends on the owner’s tax status

- If the owner is a foreigner, nonresident rules apply

If the LLC generates income effectively connected to the U.S. (ECI), the owner will be responsible for reporting these amounts through the forms applicable to nonresidents. If there is no ECI, there may be no income tax, although informational obligations may still exist.

This model is known as tax transparency, because the system “looks through” the entity and taxes the individual.

For foreign owners, this structure is extremely common, but it is also the one that creates the most confusion, as it allows for very different scenarios:

- No federal income tax if there is no ECI

- Full taxation if the activity is considered a U.S. trade or business

- Mandatory informational obligations even without revenue

Therefore, understanding that a single-member LLC does not pay taxes on its own, but the owner may have obligations, is essential to dispel the myth that “a foreign-owned LLC does not pay taxes.”

LLC with multiple owners

Treatment as a partnership

When an LLC has two or more owners and has not elected to be taxed as a corporation, the IRS by default classifies it as a partnership. Under this regime, the entity functions as a transparent tax vehicle, but with additional obligations compared to a single-member LLC.

The company usually does not pay federal income tax at the corporate level. Instead, financial results are distributed to the partners according to their ownership percentage, and each owner must report and pay taxes on their individual share.

This treatment implies that:

- The LLC files an informational partnership return

- An individual statement is issued for each partner showing their share of profits or losses

- Taxes are determined at the individual level for each owner

- If the partners are foreign, specific rules for nonresidents apply

If the LLC generates effectively connected income (ECI) in the U.S., foreign partners may be subject to taxation on their share, even without residing in the country. In such cases, mandatory withholdings may also apply to ensure tax collection.

Additionally, administrative complexity increases, as it is necessary to coordinate obligations for both the entity and each partner.

Therefore, an LLC with multiple foreign owners not only changes the taxation method but also significantly increases the level of compliance required.

LLC taxed as a corporation

Complete regime change

An LLC can also voluntarily choose to be taxed as a corporation through an election filed with the IRS. From that moment, it is no longer treated as a transparent entity and adopts a completely different regime, where the company is considered a separate taxpayer from its owners.

This represents a profound change in how taxes are calculated and in reporting obligations.

Under the corporate regime:

- The company pays tax on net income at the corporate level

- Income is no longer attributed directly to the owners

- A full corporate tax return is filed with the IRS

- Distributions to partners may trigger additional taxation

If the corporation later distributes dividends to a foreign owner, these payments are generally subject to withholding under U.S. law or applicable tax treaties.

This phenomenon is known as economic double taxation: first, the company pays tax on its profits, and then the owner may pay tax or be subject to withholding on the dividends received.

Although this regime can be advantageous in certain cases, such as reinvestment of profits or specific tax planning, it also entails greater administrative, accounting, and regulatory complexity.

For foreign owners, choosing to be taxed as a corporation should be analyzed carefully, as it completely changes the tax relationship between the company and the individual.

Practical impact

Different forms and obligations

The tax structure chosen for the LLC not only determines who pays taxes but also which forms must be filed, how often, and with which authorities. This practical impact is crucial, as many compliance errors occur precisely by applying obligations from one regime to another.

Each classification activates a different set of reports and responsibilities:

- A foreign single-member LLC classified as a disregarded entity typically requires specific informational filings, even without revenue

- An LLC treated as a partnership must file annual informational returns and individual reports for each member

- An LLC taxed as a corporation must comply with full corporate filings and possible dividend withholdings

- If there are employees, periodic labor obligations arise

- If there is activity in certain states, additional filings and payments may be required

In addition, obligations are not limited to the IRS. Depending on the case, they may involve state, labor, and regulatory authorities.

In practice, this means that two LLCs with similar activities can face completely different compliance levels simply because of their tax classification.

Therefore, before assuming “there are no taxes” or that “filing one form is enough,” it is essential to correctly identify the entity’s classification and its real effects.

Does a foreign LLC automatically pay taxes?

One of the most common beliefs among international entrepreneurs is that owning an LLC in the United States automatically means paying federal taxes. In reality, the U.S. tax system does not work that way.

The United States does not tax based on nationality or simply for having a company registered in the country. What determines tax obligations is primarily the economic connection of the income to the U.S., the structure of the entity, and the nature of the activity.

Therefore, a foreign-owned LLC can fall into very different scenarios:

- No federal income tax

- With informational obligations, but without taxation

- With partial taxation

- With full taxation similar to a local business

Understanding this logic is essential to dispel the myth that “having an LLC in the U.S. means paying taxes” or, at the opposite extreme, that “foreigners never pay taxes.”

General rule of the U.S. system

The U.S. taxes connected income, not nationality.

The basic principle of the U.S. tax system for nonresidents is to tax income that is economically connected to the country, not based on nationality or the place of company formation.

This means that:

- A foreigner can have taxable income in the U.S. even while living abroad

- They may also have no tax obligation even if they own a U.S. company

- The focus is on where the economic value is generated and where the activity occurs

This model differs from global-residency-based systems, where all taxpayer income is taxed regardless of its source.

Concept of transparent entity

Why an LLC does not always pay taxes

Many LLCs, especially single-member ones, are treated as transparent entities for tax purposes. This means the IRS does not tax the company directly but passes the results through to the owner.

Consequently:

- An LLC may not pay corporate tax

- The owner may have personal tax obligations

- If the owner is foreign, specific nonresident rules apply

- The existence of tax depends on the type of income and its connection to the U.S.

For this reason, stating that “the LLC pays taxes” or “does not pay taxes” without analyzing the structure and activity can be technically incorrect.

Importance of the type of income

Source and economic connection

Not all income related to the United States is treated the same way. The system distinguishes between income effectively connected to the country and income that is not connected.

Relevant factors include:

- Local onde os serviços são prestados

- Presença de funcionários ou agentes nos EUA

- Existência de infraestrutura física no país

- Localização do estoque ou dos ativos operacionais

- Natureza da atividade econômica

Even if clients are in the United States or payments are made in dollars, that alone does not determine taxation.

The correct analysis requires evaluating where the business is actually conducted, not just where revenue is received.

When You MUST Pay Taxes: ECI Income

The decisive factor in determining whether a foreign owner of an LLC must pay federal tax in the United States is the existence of effectively connected income, known as ECI (Effectively Connected Income).

When there is ECI, the activity is considered a business within the U.S. for tax purposes, which triggers taxation on the net income attributable to that operation. In this scenario, it does not matter if the owner lives abroad or if the company belongs to a nonresident: the U.S. tax system recognizes that economic value is being generated within its jurisdiction.

Thus, the presence of ECI completely changes the tax analysis, shifting from a possible no-tax scenario to an effective taxation regime.

What Is Effectively Connected Income

Functional definition

Effectively connected income is derived from activities that constitute a business in the United States or are closely related to it. It does not depend solely on the client’s location or the payment location, but on the real economic connection between the activity and U.S. territory.

In practice, ECI is considered when there is substantial participation in the U.S. market through operations, infrastructure, or significant presence.

Trade or Business in the United States

Substantial economic activity

For ECI to exist, the concept of Trade or Business in the United States (ETBUS) must generally be present, which means engaging in regular, continuous, and substantial economic activities within the country.

Isolated transactions are not sufficient. The IRS evaluates factors such as:

- Continuity of the activity

- Degree of business organization

- Direct participation in the U.S. market

- Use of resources located in the U.S.

When this level is reached, the associated income tends to be considered effectively connected.

Activities that generate ECI

On-site services

Inventory in the U.S.

Employees or agents

Typical situations that often generate ECI include:

- Providing services physically within the United States

- Consulting or work performed on-site in the country

- Inventory stored in U.S. territory for sale

- Distribution centers or fulfillment operations in the U.S.

- Employees, contractors, or dependent agents operating locally

- Permanent offices or facilities

The presence of people or assets in the country is one of the strongest indicators of economic connection.

Real Examples

Practical cases for clarity

Some illustrative examples:

- A foreign consultant who travels to the U.S. to serve local clients may generate ECI from work performed physically in the country.

- A foreign e-commerce company that keeps products in U.S. warehouses may generate ECI from sales of those goods.

- A foreign startup with employees working from the U.S. may also be subject to this regime.

These cases demonstrate that the determining factor is not the owner’s nationality, but the location where the economic activity takes place.

Tax consequences

Federal income tax

Mandatory filings

When the existence of ECI is confirmed, several obligations may arise:

- Payment of federal tax on attributable net income

- Filing of specific tax returns

- Possible withholdings applicable to foreigners

- More stringent accounting and documentation requirements

- Potential additional state-level obligations

In many cases, the foreign owner must report this income at the personal level if the LLC is fiscally transparent, or at the corporate level if the entity is taxed as a corporation.

Ignoring the existence of ECI is one of the most costly mistakes for foreign owners, potentially resulting in back taxes, interest, and accumulated penalties.

When there is NO ECI: online businesses operated from abroad

There is a very common scenario in which an LLC owned by a foreign individual is not subject to federal income tax in the United States: when the economic activity is carried out entirely outside the country and does not generate effectively connected income (ECI).

This is the typical case for many global digital businesses. Even if the company is registered in the U.S., invoices in dollars, or has American clients, if the economic value is generated outside U.S. territory, the income may be considered foreign-sourced and therefore not taxable at the federal level.

However, this analysis must be approached with caution. The absence of ECI depends on concrete facts about how the business operates, not just the industry in which it operates.

Non-connected income

Remote services

Operations outside the territory

Income is generally considered non-connected when:

- Services are provided entirely from outside the country

- Business management and direction take place outside the U.S.

- There are no employees, offices, or infrastructure in the country

- There is no inventory or operational assets located in the U.S.

- Strategic decisions are made outside U.S. territory

In this context, the U.S. tax system does not consider that there is a business in the United States, even if the clients are located there.

Common scenarios

SaaS

Digital consulting

Ecommerce without inventory in the U.S.

Models commonly classified as not having ECI include:

- Software companies or SaaS platforms operated from abroad

- Consultants, freelancers, or digital agencies working remotely

- Sale of courses, digital products, or online services

- Ecommerce with international dropshipping without storage in the U.S.

- Businesses based on intellectual property exploited outside the country

In these cases, the location of the customer or market alone does not determine taxation.

Limitations

Changes that may generate ECI

Risk of incorrect interpretation

A business that initially does not generate ECI may begin to do so if its operations change. Some situations that may alter the analysis include:

- Hiring employees or representatives in the U.S.

- Opening offices or physical facilities

- Maintaining inventory in U.S. territory

- Providing services in person within the country

- Using dependent agents with authority to close contracts

Additionally, incorrect interpretation of the rules is a relevant risk. Many entrepreneurs believe that an “online business” automatically means “no taxes,” which is not always true.

For this reason, periodically assessing how the activity is actually conducted is essential to maintain tax compliance and avoid future issues.

Form 1040NR: when it is required

The Form 1040NR (U.S. Nonresident Alien Income Tax Return) is the personal income tax return that certain nonresident foreigners must file when they obtain taxable income in the United States. This form is essential because, in many LLC structures with a foreign owner, the tax obligation does not fall on the company, but directly on the individual.

Understanding when the 1040NR is required allows you to correctly distinguish between the obligations of the entity and the owner, avoiding the common mistake of believing that complying with corporate filings is sufficient.

What is the 1040NR

Personal return for nonresidents

Form 1040NR is the federal return used by the IRS for nonresident foreigners to report U.S.-source income subject to taxation.

Through this form, the following are reported:

- Taxable income earned in the U.S.

- Allowable deductions related to that income

- Calculated federal tax

- Withholdings made during the year

- Application of tax treaties, when applicable

It does not replace the company’s filings nor is it part of them. It is an individual obligation.

Why it is not the LLC

Difference between individual and entity

Many single-member LLCs owned by foreign individuals are treated as transparent entities for tax purposes. This means that the IRS does not tax the company as a separate taxpayer, but instead attributes the results directly to the owner.

Consequently:

- The LLC may have its own informational obligations

- The owner may have additional personal tax obligations

- Both may exist simultaneously and must be fulfilled separately

Confusing the responsibility of the company with that of the individual is one of the most common mistakes in international compliance.

Relationship with ECI income

Reporting personal income in the U.S.

The 1040NR is generally required when the foreign owner earns income effectively connected to the United States. In this case, they must report the net income attributable to the economic activity carried out in the country.

It may also be required when there are other types of U.S.-source income subject to taxation, even if not directly derived from the LLC.

The form allows the calculation of the tax due and determines whether there are additional amounts to be paid or refunded.

How income from a transparent LLC is reported

Tax flow to the owner

In a single-member LLC classified as a disregarded entity, the income does not remain within the company for tax purposes. It is treated as the owner’s income.

Therefore:

- If there is ECI, the foreign owner reports these amounts on their personal tax return

- The LLC functions as an operational vehicle, not as a separate taxpayer

- The company’s accounting serves as the basis for the individual return

This tax flow characterizes the transparency model typical of many LLCs owned by foreign individuals.

Consequences of not filing

Penalties and cumulative issues

Failing to file Form 1040NR when required may lead to significant consequences:

- Penalties for non-compliance

- Interest on unpaid taxes

- Accumulation of tax liabilities

- Risk of audits or additional requirements

- Future issues in immigration or financial processes

Additionally, failure to report may make future compliance more difficult, as the IRS may estimate taxes based on incomplete information.

Understanding when this form is required is essential to maintaining proper tax compliance as a foreign owner of an LLC in the United States.

SUPPLEMENTARY INFORMATION: BOIR (FinCEN): obligation even without paying taxes

The BOIR (Beneficial Ownership Information Report) is a federal regulatory obligation that many LLCs in the United States must comply with regardless of whether they pay taxes or generate revenue. This report is part of corporate transparency and financial crime prevention rules, and its requirement does not depend on the company’s tax situation or that of its owner.

For foreign owners, this is particularly relevant, as an LLC may have no federal income tax liability and still be required to file the BOIR.

What is the BOIR

Beneficial ownership report

The BOIR identifies the individuals who directly or indirectly own or control a company registered in the U.S. These individuals are referred to as beneficial owners.

The objective is to prevent corporate structures from being used to conceal the identity of the true controllers.

Typically, the following must be reported:

- Owners with a significant ownership interest in the company

- Individuals with substantial control over the entity

- In some cases, those involved in the formation of the company

The report includes basic personal information and identification documents of the beneficial owners.

FinCEN vs IRS

Different authorities

The BOIR is not filed with the IRS nor is it part of the tax system. It is submitted to the FinCEN (Financial Crimes Enforcement Network), an agency of the U.S. Department of the Treasury responsible for combating money laundering and financial crimes.

This means that:

- It is not a tax return

- It does not involve the calculation or payment of taxes

- Its purpose is regulatory

- Non-compliance follows different rules than tax obligations

Confusing this obligation with taxes is a common mistake.

Who must file

Companies registered in the U.S.

The obligation applies to most entities created or registered to operate in the United States, including many LLCs owned by foreign individuals.

It does not depend on:

- Existence of revenue

- Presence of employees

- Operational activity

- Owner’s residency

The determining factor is the legal existence of the company within the U.S. system.

Deadlines and penalties

Consequences of non-compliance

Deadlines vary depending on the company’s formation date and any changes to the reported information.

Failure to comply may result in:

- Significant civil penalties

- Accumulating fines per day of delay

- Potential criminal consequences in severe cases

- Difficulties proving compliance to banks and partners

Ignoring this obligation may create significant risks even without economic activity.

Why it is not a tax

Regulatory nature

The BOIR does not require payment to the government nor the calculation of taxes. Its purpose is to ensure transparency regarding who controls the company.

Even so, its importance is similar to that of a tax obligation because:

- It is mandatory

- It carries penalties for non-compliance

- It may affect the company’s operations

- It is part of the global financial compliance system

In summary, not paying taxes does not mean the absence of obligations. The BOIR is a clear example of this.

Other forms that may apply

In addition to Form 1040NR and the BOIR, there are other federal forms that may be required for an LLC in the United States with foreign owners. These reports depend primarily on the entity’s tax classification, the number of members, the economic activity, and the existence of employees or specific transactions.

Not all LLCs are required to file the same forms. Applying a generic model is a common mistake and can lead to both non-compliance and the submission of unnecessary documentation.

Form 5472 + pro forma 1120

Typical obligation for foreign-owned LLCs

For many foreign-owned single-member LLCs classified as disregarded entities, the main obligation before the IRS is to file Form 5472 along with a pro forma Form 1120.

This report is informational and does not calculate tax. Its purpose is to report transactions between the LLC and its foreign owner or related parties.

It is required when at least one reportable transaction occurs, even without operational revenue. Among the most common are:

- Capital contributions from the owner

- Withdrawals or distributions of funds

- Loans between the owner and the company

- Payment of personal expenses with LLC funds or vice versa

- Transactions with related companies abroad

Failure to comply may result in significant penalties for each year not reported, regardless of whether any tax is due.

Forms for partnerships

If there are multiple partners

When an LLC has two or more owners and is treated as a partnership, it must file an annual informational return reporting its results.

Under this regime:

- The entity reports total results

- Each partner receives their proportional share

- Owners report their share individually

If there are foreign partners and the activity generates income effectively connected to the U.S., mandatory withholdings and additional obligations may apply.

Employment obligations

If there are employees

Hiring employees in the United States creates an entirely new set of tax and regulatory responsibilities.

Among them:

- Periodic reports on wages and withholdings

- Annual informational forms for employees

- Obligations related to Social Security and Medicare

- Federal and state payroll taxes

These requirements are independent of the owner’s nationality and imply ongoing compliance throughout the entire year.

Additional reports

Depending on the business

Some activities may require additional forms or registrations, for example:

- Payments to independent contractors in the U.S.

- Specific financial transactions

- Activities regulated by federal or state agencies

- Situations arising from tax treaties

For this reason, applicable forms must be determined individually, according to the company’s operational reality.

State-level obligations that many foreigners overlook

In addition to federal obligations, an LLC in the United States may be subject to tax and administrative requirements at the state level. This is one of the most overlooked aspects by foreign owners, especially when the company does not generate revenue in the U.S. or operates digitally from abroad.

However, states have autonomy to impose their own taxes, fees, and reporting requirements. These obligations often exist simply because the company is registered or maintains activities that create an economic connection with the state.

Ignoring state compliance can result in consequences as serious as federal non-compliance, even without any income tax due.

Franchise tax and minimum taxes

Independent of revenue

Many states impose a franchise tax or a minimum annual tax for the right to operate as a legal entity within their jurisdiction. This payment does not necessarily depend on profit or business volume.

It may be required even when:

- The company had no revenue

- There was no operational activity

- There are no employees

- The business is conducted from abroad

The amounts and rules vary widely between states.

Annual reports

Legal maintenance

Most states require the filing of a periodic report called an annual report to keep the company active.

This report typically includes:

- Updated entity information

- Information about responsible parties or managers

- Registered address

- Confirmation of continued existence

This is an administrative obligation, not a tax one, but it is essential for the legal existence of the company.

Nexus in other states

Operating outside the state of formation

An LLC may be registered in one state and still have obligations in others if there is nexus, meaning a sufficient economic connection with another jurisdiction.

Nexus may arise when the company:

- Has employees or contractors in another state

- Maintains inventory or assets in that territory

- Operates physically there

- Exceeds certain levels of economic activity

In this case, the company may have to comply with additional obligations in that state.

Registration as a foreign entity

Additional requirements

When an LLC operates in a state different from the one in which it was formed, it may be necessary to register it as a foreign entity in that state.

This may involve:

- Formal application for authorization to operate

- Payment of additional fees

- Appointment of a local registered agent

- Compliance with specific reports and obligations

This requirement is common when there is a relevant physical or economic presence outside the original state.

Consequences of non-compliance

Suspension or dissolution

Failure to comply with state obligations may result in:

- Fines and accumulated charges

- Loss of good standing

- Administrative suspension of the company

- Involuntary dissolution

- Difficulties operating with banks and partners

Even if the company continues to formally exist, a non-compliant entity may face serious operational obstacles.

For this reason, the tax analysis of a foreign-owned LLC should always consider the state level, not just the federal level.

Obligations even without paying taxes

One of the biggest misconceptions about foreign-owned LLCs in the United States is believing that if there is no federal tax due, there are also no legal or regulatory obligations. In practice, many companies operate with “zero tax,” but this does not mean the absence of responsibilities.

The U.S. system clearly distinguishes between tax, informational, regulatory, and corporate obligations. An LLC may be subject to several of them even without revenue or without ECI.

Informational reports

Federal and state

Various forms exist solely to provide information to authorities, not to calculate tax.

Among the most common:

- Informational filings to the IRS regarding the company’s structure or operations

- Reports involving foreign owners or related parties

- Mandatory state maintenance reports

- Regulatory reports depending on the type of activity

The absence of these reports may result in penalties even without any tax due.

Corporate compliance

Maintaining the entity active

Every LLC must comply with formal requirements to preserve its legal existence.

This may include:

- Maintaining a valid registered agent

- Renewing the company periodically

- Preserving essential corporate documentation

- Updating official information when necessary

- Complying with governance rules

Failure to comply may lead to the loss of active status and limit the company’s operational capacity.

Banking requirements

KYC and compliance

Financial institutions apply strict KYC and anti-money laundering controls, especially for companies with foreign owners.

Even without tax due, they may require:

- Up-to-date company documentation

- Proof of regulatory compliance

- Information about beneficial owners

- Details of the business model

- Activity consistent with the declared profile

Lack of compliance may result in restrictions, account freezes, or account closure.

The reality of “zero tax”

It does not mean zero obligations

Many nonresident-owned LLCs legally operate without paying federal income tax, but they are still required to:

- File mandatory reports

- Comply with state requirements

- Maintain the company in good standing

- Meet regulatory and banking requirements

The main risk is not the absence of tax, but the false perception that there are no obligations at all.

Risks of believing the “pays nothing” myth

The idea that a foreign-owned LLC “does not pay taxes in the U.S.” has become common in simplified content. While it may be true in specific scenarios, interpreting it as a total absence of obligations is a potentially costly mistake.

The main risk is not the lack of federal income tax, but rather the neglect of informational, regulatory, and corporate obligations that remain required.

Informational penalties

Various mandatory forms are informational, but the penalties for failing to file them can be significant.

Penalties may occur due to:

- Failure to file a required form

- Filing after the deadline

- Providing incomplete or incorrect information

- Ignoring subsequent notices

Important: these penalties do not depend on whether any tax is due.

Banking issues

Financial institutions continuously monitor compliance risk.

Possible consequences:

- Requests for additional documentation

- Operational restrictions

- Freezing of funds

- Account closures

- Difficulty opening new accounts

For digital businesses, this is usually the most immediate impact.

Accrued interest

When there is a tax obligation, for example, in the presence of ECI, delays may result in:

- Interest from the original due date

- Penalties for late filing

- Penalties for late payment

- Adjustments after tax review

These charges increase over time, making compliance progressively more expensive.

Loss of good standing

State non-compliance may lead to the loss of the company’s active status.

This may affect:

- Validity of contracts

- Expansion into other states

- Banking relationships

- Audit processes

Restoring the status usually requires retroactive payments and additional procedures.

Operational and reputational impact

In addition to formal sanctions, non-compliance may compromise business operations.

Among the indirect effects:

- Delays in international operations

- Loss of partner trust

- Difficulty scaling

- Risks in company sale processes

- Increased future regulatory scrutiny

The result may be exactly the opposite of what was expected: a total cost much higher than complying properly from the beginning.

Common mistakes

“I don’t live in the U.S., I don’t owe anything”

This is probably the most widespread myth among foreign LLC owners. The U.S. tax system is not based on the owner’s geographic residence, but rather on the economic connection of the income and the entity’s informational obligations.

A person may live permanently outside the U.S. and still:

- Have income subject to federal taxation

- Be required to file a personal return (for example, Form 1040NR)

- Need to comply with mandatory LLC informational forms

- Be subject to state-level obligations

- Face penalties for non-compliance even without tax due

Place of residence does not eliminate tax or regulatory responsibilities when there are connections to the U.S. system.

Confusing income in dollars with income in the U.S.

Billing in dollars, receiving payments from U.S. clients, or using U.S. financial platforms does not automatically mean that the income is U.S.-sourced or that there is ECI.

The decisive factor is where the economic activity that generates the income takes place. For example:

- Services performed physically outside the U.S. are generally considered foreign-sourced

- Activities carried out within U.S. territory may generate ECI

- The location of servers, inventory, or employees may have an impact

- Contracts and the way services are executed are also relevant

Basing the analysis solely on currency is a mistake that can lead both to unnecessary tax payments and to failure to comply with actual obligations.

Ignoring state obligations

Many owners focus only on the IRS and overlook that states have their own tax and corporate systems.

Even without federal tax, the LLC may need to:

- Pay franchise tax or a minimum annual tax

- File annual reports

- Renew corporate registrations

- Maintain good standing status

- Register in other states if there is operational nexus

State non-compliance may lead to administrative suspension or dissolution of the company, directly affecting its ability to operate.

Not considering tax treaties

The U.S. maintains tax treaties to avoid double taxation with various countries. These agreements may affect:

- The taxation of certain types of income

- The applicable tax rates

- The rules regarding permanent establishment

- Withholding requirements

- Mechanisms to avoid double taxation

Ignoring an applicable treaty may result in excessive tax payments or improper structuring of operations.

However, applying a treaty requires formal requirements and specific documentation.

Thinking that the EIN is sufficient

Obtaining an EIN is often seen as the final step to “legalize” an LLC, when in reality it is only the entity’s tax identification number with the IRS.

The EIN does not:

- Define the tax classification

- Eliminate the need to file returns

- Replace state-level obligations

- Automatically authorize any activity

- Guarantee regulatory compliance

An LLC may have an active EIN and still be completely out of compliance if it does not meet other legal obligations.

Comprehensive checklist

Key factors to review

Before assuming that a nonresident-owned LLC “does not pay taxes,” it is essential to comprehensively analyze its tax and operational situation. There is no single answer, as the treatment depends on multiple interrelated variables.

Among the most relevant factors are:

- LLC tax classification (disregarded entity, partnership, or corporation)

- Number and profile of the owners

- Nature of the economic activity

- Location where services are performed or value is generated

- Existence of employees, agents, or infrastructure in the U.S.

- Presence or absence of specific tax elections

- Owner’s country of residence and potential tax treaties

A superficial assessment based solely on the company’s formation may lead to incorrect conclusions.

Indicators of ECI

Identifying the existence of effectively connected income (ECI) is one of the most critical points, as it determines whether there will be federal income taxation.

Some indicators that may suggest ECI include:

- Providing services within U.S. territory

- Significant or recurring physical presence in the U.S.

- Inventory stored or distributed from within the country

- Employees or dependent agents operating in the U.S.

- Ongoing business activity directed at the U.S. market from within U.S. territory

- Existence of an office, branch, or permanent establishment

No single factor is necessarily decisive. The analysis must consider the full set of circumstances.

Signs of non-compliance

There are indications that an LLC may be out of compliance even without the owner realizing it:

- Failure to file mandatory informational forms for several years

- Lack of awareness of the entity’s actual tax classification

- Failure to pay franchise tax or file state annual reports

- Lack of proper accounting or financial records

- Failure to assess personal obligations such as Form 1040NR

- Changes in the business model without subsequent tax review

Ignoring these signs increases the risk of accumulated penalties and future issues.

When to seek professional advice

It is advisable to conduct a professional review when:

- There are doubts about the existence of ECI

- The business has grown or changed significantly

- There are operations in multiple states

- There are plans to hire employees or maintain inventory in the U.S.

- Returns were not filed in previous years

- The owner needs certainty to scale or attract investment

Preventive advisory services usually cost much less than correcting accumulated non-compliance and allow the business to operate with greater legal and tax certainty.

Conclusion

Summary of myth vs reality

Importance of individual analysis

Preventive approach

Owning an LLC in the United States as a nonresident does not automatically mean paying federal tax, but it also does not mean a complete absence of obligations. The U.S. tax system is primarily based on the economic connection of income with the country, not on the nationality or place of residence of the owner.

The myth that “foreigners don’t pay anything” arises from oversimplifications that ignore essential factors such as the existence of effectively connected income (ECI), the LLC’s tax structure, federal informational obligations, state requirements, and regulatory reports such as the BOIR. Depending on these variables, an LLC may operate with a minimal tax burden or face a level of compliance similar to any business operating within the U.S.

Each situation must be analyzed individually. Two seemingly identical companies may have completely different tax treatments due to their business model, economic presence, ownership structure, or the owner’s country of residence.

A preventive approach allows you to anticipate obligations, avoid penalties, and use the LLC as a legitimate instrument to operate globally. The key question is not only whether there is tax to pay, but understanding precisely what applies in each case and complying correctly.

In an increasingly strict regulatory environment with greater international information exchange, transparency and compliance not only reduce legal and financial risks but also strengthen the business’s long-term stability and credibility.

Tax assessment for nonresident-owned LLCs

If you own an LLC in the United States and are a nonresident, understanding your exact tax and regulatory obligations is not optional: it is essential to operate safely and avoid issues that may arise years later.

A specialized tax assessment analyzes your specific situation, LLC structure, type of activity, economic presence, country of residence, and personal obligations to determine precisely:

- Whether your business generates or may generate ECI

- Which federal forms must actually be filed

- Whether there are personal obligations such as Form 1040NR

- Which state requirements apply

- Whether the current structure is efficient or presents hidden risks

- How to prevent penalties, banking restrictions, or operational issues

Many foreign-owned LLCs operate for years under incorrect assumptions until a business change, banking review, or official notice reveals accumulated irregularities.

Acting preventively reduces costs, brings clarity, and allows the LLC to be used as a strategic tool for international expansion.

If you are seeking legal and tax certainty for your business, a professional review can transform an uncertain scenario into a solid structure prepared for long-term growth.

Official sources for reference

The following publications and legal sections constitute the regulatory basis for the topics covered in this article. Direct consultation is recommended to validate the information:

IRS publications:

- Publication 519 (U.S. Tax Guide for Aliens): Comprehensive guide on the taxation of nonresident foreigners, including criteria for tax residency, the concept of Effectively Connected Income (ECI), and source-of-income rules.

- Available at: www.irs.gov/pub/irs-pdf/p519.pdf

- Publication 541 (Partnerships): Details the tax obligations for partnerships, including LLCs with multiple members that do not elect to be taxed as corporations.

- Available at: www.irs.gov/pub/irs-pdf/p541.pdf

- Form 5472 – Instructions: Official document specifying which entities must file Form 5472, which transactions are reportable, and penalties for non-compliance.

- Available at: www.irs.gov/instructions/i5472

- Form 1040NR – Instructions: Official guide for nonresident income tax returns, detailing which income must be reported and how to calculate the tax.

- Available at: www.irs.gov/instructions/i1040nr

Code and regulations:

- Internal Revenue Code Section 864(c): Defines the concept of Effectively Connected Income (ECI) and establishes the criteria to determine whether a nonresident’s income is connected to a business in the U.S.

- Treasury Regulation § 1.6011-4: Requirement to disclose positions based on tax treaties through Form 8833.

- Treasury Regulation § 301.7701-1 to -3: Entity classification for tax purposes (check-the-box regulations), the basis for treating an LLC as a disregarded entity or partnership.

BOIR (Beneficial Ownership Information Report):

- FinCEN – Beneficial Ownership Information: Official portal with guides, deadlines, and requirements for filing the BOIR.

- Available at: www.fincen.gov/boi

Frequently asked questions (FAQ)

Do I need to pay taxes if my LLC has no income in the U.S.?

Not necessarily. A nonresident-owned LLC only pays federal income tax when it generates effectively connected income (ECI) with the U.S. or when it elects to be taxed as a corporation. However, the absence of income does not eliminate other obligations, such as informational filings, regulatory reports, and state requirements.

In other words, “not paying taxes” does not mean “doing nothing.”

Can I have an LLC in the U.S. without living there?

Yes. U.S. law allows foreigners to form and own LLCs without residing, traveling, or having immigration status in the country. Many businesses are operated entirely from abroad.

What matters is not the owner’s residence, but where the economic activity takes place and which obligations are triggered.

Do I need an ITIN to have an LLC as a foreigner?

Not always. A foreigner can open an LLC and obtain an EIN without having an ITIN or SSN. However, an ITIN may be required if the owner needs to file a personal return with the IRS, such as Form 1040NR, claim tax treaty benefits, or comply with other individual obligations.

Do I need to pay taxes in my country of residence?

In most cases, yes. Taxation in the U.S. and in the country of residence are independent systems. Even if the LLC does not pay U.S. federal tax, the owner may need to report the income locally.

Tax treaties may avoid double taxation, but they do not automatically eliminate the obligation to report.

Does the BOIR involve paying taxes?

No. The BOIR is a regulatory report required by FinCEN to identify the company’s beneficial owners. It is not a tax form and does not calculate tax.

Its purpose is corporate transparency and the prevention of financial crimes, but non-compliance may result in significant penalties.

What happens if I do not file the required forms?

The consequences may include:

- Informational penalties for each unreported year

- Interest and penalties if there is tax due

- Notices from the IRS or state authorities

- Loss of good standing

- Banking or operational issues

- Greater difficulty in future compliance

Even without profit, the risk still exists.

Does charging U.S. clients automatically create tax liability?

No. Having U.S. clients or billing in dollars does not automatically mean there is ECI. The decisive factor is where the economic activity that generates the income takes place.

Services performed entirely outside the U.S. are generally considered foreign-sourced, while activities carried out within the country may generate taxation.

Can I hire employees in the U.S. as a nonresident?

Yes, but this creates significant additional obligations. A company with employees in U.S. territory must comply with labor, tax, and social security rules, regardless of the owner’s residence.

Additionally, the presence of employees usually indicates substantial economic activity in the U.S., which may generate ECI.

How do I know if my LLC has ECI?

There is no single test. The IRS evaluates factors such as physical presence, services performed in the country, local employees or agents, inventory in the U.S., or ongoing business operations from within U.S. territory.

If in doubt, a technical assessment is recommended to avoid errors that may result in improper tax payments or non-compliance.

How do the U.S. determine whether income is U.S.-sourced or foreign-sourced?

The U.S. tax system uses specific “source of income” rules. In general:

- Services are taxed based on where they are physically performed

- Interest, dividends, and royalties depend on the payer or the asset

- Sale of goods may depend on the place of production and delivery

- Real estate income is taxed where the property is located

This classification is essential because nonresidents are taxed only on U.S.-source income or effectively connected income.

What does “trade or business in the United States” mean in practice?

It is the criterion used by the IRS to determine whether there is sufficient economic activity within the country to generate ECI. There is no automatic definition; the substance of the operation is analyzed.

In practice, it involves regular, continuous, and significant participation in business activities in the U.S.

How do contracts influence taxation?

Contracts can be decisive because they indicate where the service is performed, who assumes risks, and where delivery takes place. The IRS analyzes both the contract content and its actual execution.

A contract stating that the service occurs outside the U.S. does not provide protection if, in practice, it is carried out within the country.

Can the tax situation change from one year to another?

Yes. The taxation of a foreign-owned LLC may vary depending on operational changes. Hiring employees in the U.S., opening an office, or maintaining inventory can transform a non-ECI scenario into a taxable one.

Each tax year must be analyzed separately.

What is double taxation and when does it occur?

It occurs when the same income is taxed by two different countries, such as the U.S. and the owner’s country of residence. Tax treaties usually provide mechanisms to avoid this duplication.

Do digital platforms influence taxation?

Operating through marketplaces or platforms does not automatically determine taxation, but it may indicate where the economic activity takes place. The use of logistics centers in the U.S., for example, may create a relevant economic presence.

What happens if the owner changes tax residency?

A change to U.S. tax residency completely alters the tax regime, including worldwide income and broader reporting obligations.

How do tax obligations relate to banks?

Financial institutions apply strict compliance controls. They may require documentation proving that the company is compliant. Inconsistencies may result in restrictions or account closures.

What is good standing and why is it important?

Good standing is the status confirming that the company is compliant with the state. It is required for various corporate and financial operations.

Are there differences between states regarding taxes for foreign-owned LLCs?

Yes. Each state has its own rules. Some impose high minimum taxes regardless of revenue, while others have lighter requirements.